Understanding 2026 Medicare Changes: A Comprehensive Guide for U.S. Seniors

Anúncios

Understanding 2026 Medicare Changes: A Comprehensive Guide for U.S. Seniors

As we approach 2026, many U.S. seniors are beginning to wonder about the potential 2026 Medicare Changes and how these updates might impact their healthcare coverage, costs, and overall well-being. Medicare, a cornerstone of healthcare for millions of Americans aged 65 and older, as well as younger individuals with certain disabilities, is subject to periodic adjustments to ensure its long-term viability and to adapt to evolving healthcare needs and economic realities. Navigating these changes can be complex, but understanding them proactively is crucial for making informed decisions about your health and financial future.

Anúncios

This comprehensive guide aims to demystify the anticipated 2026 Medicare Changes, providing U.S. seniors with a clear overview of what to expect, how these changes might affect various aspects of Medicare (Parts A, B, C, and D), and practical steps you can take to prepare. From potential shifts in premium costs and deductibles to modifications in covered services and prescription drug benefits, staying informed is your best defense against unexpected challenges. We will delve into the legislative landscape, economic factors, and demographic trends that often drive these adjustments, offering a holistic perspective on the future of Medicare.

Anúncios

The Evolving Landscape of Medicare: Why Changes Occur

Medicare is not a static program; it is continually evaluated and adjusted by Congress and the Centers for Medicare & Medicaid Services (CMS) to address a multitude of factors. These factors include advancements in medical technology, the rising cost of healthcare services, demographic shifts (such as the aging baby boomer population), and the financial health of the Medicare trust funds. The 2026 Medicare Changes are likely to be influenced by these ongoing considerations, aiming to balance the provision of essential healthcare services with fiscal responsibility.

One of the primary drivers of Medicare changes is the financial sustainability of the program. Medicare is funded through a combination of payroll taxes, beneficiary premiums, and general revenue. As the population ages and healthcare costs continue to rise, maintaining the solvency of the Medicare Trust Funds becomes a significant challenge. Consequently, policymakers often explore various avenues to ensure the program can continue to meet the needs of future generations. These avenues can include adjustments to beneficiary contributions, changes to provider reimbursement rates, and initiatives to promote more efficient healthcare delivery.

Technological advancements also play a crucial role. New medical treatments, diagnostic tools, and pharmaceutical innovations often come with a high price tag. Medicare must adapt to these advancements, deciding which new services to cover and how to reimburse providers for them. This process can lead to changes in covered benefits, formulary updates for prescription drugs, and sometimes, new cost-sharing arrangements for beneficiaries. The goal is to ensure access to cutting-edge care while managing overall program expenditures.

Furthermore, legislative actions can introduce significant modifications to Medicare. Congress frequently debates and passes legislation that directly impacts the program, ranging from broad reforms to specific policy adjustments. These legislative efforts are often a response to public demand, economic pressures, or the findings of various expert commissions and advisory bodies. Staying abreast of potential legislative discussions is an important part of understanding anticipated 2026 Medicare Changes.

Demographic shifts, particularly the increasing number of seniors, place additional strain on the Medicare system. As more individuals become eligible for Medicare, the beneficiary base grows, increasing demand for services. This growth necessitates careful planning and potential adjustments to ensure that the program can adequately serve all eligible individuals without compromising quality or access. The aging population also means a greater prevalence of chronic conditions, which typically require more intensive and costly care, further influencing the need for program adjustments.

In essence, the 2026 Medicare Changes will not emerge in a vacuum. They will be the product of a complex interplay of economic forces, demographic realities, legislative priorities, and healthcare innovation. For U.S. seniors, understanding these underlying dynamics can provide valuable context for interpreting and preparing for the upcoming adjustments.

Anticipated Changes to Medicare Part A: Hospital Insurance

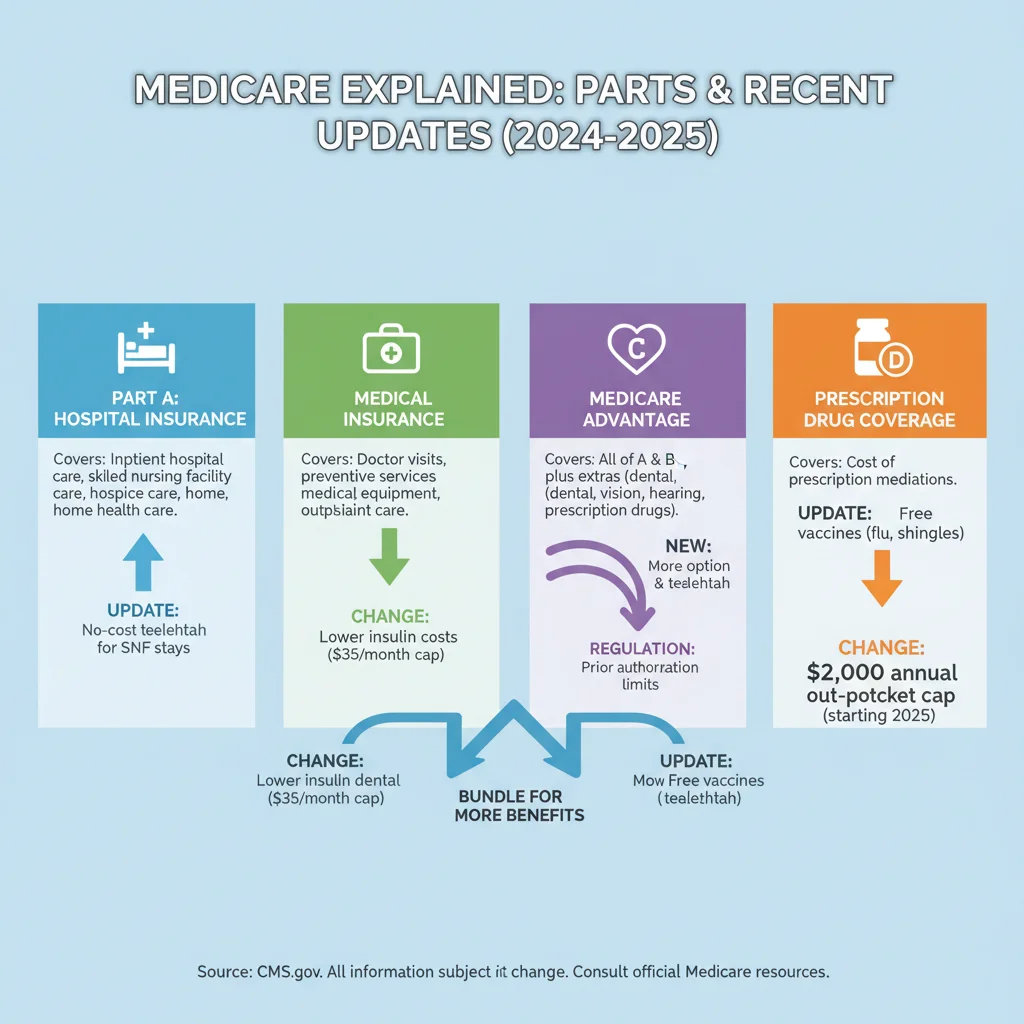

Medicare Part A primarily covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health services. While Part A is often premium-free for most beneficiaries who have paid Medicare taxes through employment for a sufficient period, it does involve deductibles and coinsurance. The 2026 Medicare Changes for Part A might focus on adjusting these cost-sharing amounts or refining coverage criteria.

Historically, Part A deductibles and coinsurance amounts are reviewed annually and can be adjusted based on various factors, including the average cost of healthcare services. For 2026, it is possible we could see slight increases in the inpatient hospital deductible, which beneficiaries pay for each benefit period. Similarly, coinsurance amounts for extended hospital stays or skilled nursing facility care might also be revised. These adjustments are typically made to align beneficiary contributions with the rising costs of inpatient care.

Another area that could see adjustments relates to the criteria for skilled nursing facility (SNF) coverage. Medicare Part A covers SNF care under specific conditions, usually following a qualifying hospital stay. Policymakers might consider refining these criteria to ensure that SNF services are utilized appropriately and efficiently. This could involve stricter adherence to medical necessity guidelines or modifications to the length of covered stays, though any such changes would likely be implemented with careful consideration for patient needs.

Hospice care, another vital component of Part A, generally has very few out-of-pocket costs for beneficiaries. While major overhauls to hospice benefits are less common, minor adjustments to reimbursement rates for hospice providers could indirectly influence the availability or scope of services in some areas. However, the fundamental structure of hospice coverage under Part A is expected to remain largely consistent, continuing to provide comprehensive support for end-of-life care.

Home health services covered by Part A are also subject to review. As healthcare increasingly shifts towards home-based care, there might be discussions around expanding certain home health benefits or adjusting the requirements for eligibility. Conversely, efforts to curb potential fraud and abuse in home health could lead to more stringent oversight and documentation requirements for providers. These changes, if implemented, would aim to ensure that beneficiaries receive necessary care in the most appropriate and cost-effective settings.

For seniors, actively monitoring the official announcements from CMS regarding Part A deductibles and coinsurance is paramount. These figures are usually released well in advance of the new calendar year, providing ample time for financial planning. Understanding these potential 2026 Medicare Changes in Part A will help you anticipate out-of-pocket expenses for hospitalizations and skilled nursing care.

Projected Shifts in Medicare Part B: Medical Insurance

Medicare Part B covers medically necessary services such as doctor visits, outpatient care, durable medical equipment, and preventive services. Unlike Part A, most beneficiaries pay a monthly premium for Part B, along with an annual deductible and coinsurance. The 2026 Medicare Changes in Part B often have the most direct and noticeable financial impact on seniors.

The Part B premium is a significant concern for many seniors. This premium is typically deducted directly from Social Security benefits. While a ‘hold harmless’ provision often protects current beneficiaries from large premium increases if their Social Security cost-of-living adjustment (COLA) is insufficient to cover the rise, this protection does not apply to all beneficiaries (e.g., those new to Medicare, those with higher incomes, or those not receiving Social Security benefits). The standard Part B premium is influenced by the overall costs of Part B services and the financial health of the program. Therefore, it is highly probable that we will see an adjustment to the standard Part B premium for 2026, potentially an increase, though the exact amount will depend on various economic projections and legislative decisions.

The Part B deductible is another area likely to see changes. Similar to Part A, the Part B deductible is reviewed annually and can be adjusted upwards to reflect rising healthcare costs. After meeting the deductible, beneficiaries typically pay 20% of the Medicare-approved amount for most Part B services. Any increase in the deductible would mean beneficiaries pay more out-of-pocket before their Medicare coverage kicks in for the 80% share.

Beyond premiums and deductibles, the scope of covered services under Part B could also be subject to refinement. With ongoing debates about mental health parity and access to telehealth, there might be expansions or clarifications in these areas. For instance, increased coverage for certain mental health therapies or a more permanent integration of telehealth services post-pandemic could be part of the 2026 Medicare Changes. Conversely, new guidelines for certain medical procedures or diagnostic tests might be introduced, affecting what is covered and under what conditions.

Preventive services, which are largely covered at 100% under Part B, are a key focus of public health initiatives. While major reductions in preventive care are unlikely, there could be updates to recommended screenings or the introduction of new preventive services based on evolving medical guidelines. Encouraging preventive care remains a cost-effective strategy for improving senior health and reducing future acute care needs.

For higher-income beneficiaries, the Income-Related Monthly Adjustment Amount (IRMAA) could also see changes. IRMAA is an additional amount added to the Part B (and Part D) premium based on income. The income thresholds for IRMAA are adjusted annually. For 2026, these thresholds could be revised, potentially affecting more beneficiaries or altering the amount of the surcharge for those already subject to it. Understanding these potential income-related adjustments is vital for financial planning.

In summary, Part B is often where beneficiaries feel the most direct impact of Medicare changes. Closely monitoring announcements regarding premiums, deductibles, and covered services will be essential for seniors preparing for the 2026 Medicare Changes.

Potential Updates to Medicare Part C: Medicare Advantage Plans

Medicare Part C, known as Medicare Advantage, offers an alternative way to receive Medicare benefits. These plans are offered by private insurance companies approved by Medicare and must cover all the services that Original Medicare (Parts A and B) covers, except for hospice care. Many Medicare Advantage plans also offer additional benefits not covered by Original Medicare, such as vision, dental, hearing, and prescription drug coverage. The 2026 Medicare Changes for Part C will largely revolve around plan offerings, benefits, and provider networks.

One of the most dynamic aspects of Medicare Advantage is the annual negotiation between private insurers and CMS regarding plan benefits and reimbursement rates. For 2026, we can anticipate continued evolution in the types of supplemental benefits offered. Plans might introduce new perks to attract beneficiaries, such as expanded telehealth services, fitness programs, or even healthy food allowances. Conversely, some plans might scale back less popular benefits or adjust cost-sharing for certain services to manage costs.

Provider networks are another critical component of Medicare Advantage plans. These networks can change annually, meaning your current doctors or hospitals might or might not be included in the same plan next year. Seniors enrolled in Medicare Advantage should meticulously review their plan’s Annual Notice of Change (ANOC) and Evidence of Coverage (EOC) for 2026 to ensure their preferred providers remain in-network. Any significant 2026 Medicare Changes to network composition could necessitate switching plans during the Annual Enrollment Period.

Premiums for Medicare Advantage plans also vary widely. While many plans offer a $0 monthly premium (beyond the Part B premium), others charge an additional amount. These premiums are subject to annual review and can change for 2026. Beneficiaries should compare premiums, deductibles, copayments, and maximum out-of-pocket limits when evaluating their options. The trend towards higher enrollment in Medicare Advantage may continue, leading to increased competition among plans, which could, in some cases, result in more competitive pricing or enhanced benefits. However, regulatory changes or shifts in reimbursement models could also influence these costs.

CMS often implements new regulations or guidelines for Medicare Advantage plans to ensure quality and protect beneficiaries. The 2026 Medicare Changes could include stricter requirements for plan marketing, improved transparency in benefit explanations, or enhanced oversight of utilization management practices. These measures are typically designed to ensure beneficiaries understand their coverage fully and receive appropriate care without undue administrative hurdles.

Special Needs Plans (SNPs), a type of Medicare Advantage plan tailored to individuals with specific chronic conditions, institutionalized individuals, or those eligible for both Medicare and Medicaid, are also subject to ongoing adjustments. There might be new requirements for SNPs or expansions in the types of conditions they can cover, aiming to provide more targeted and coordinated care for vulnerable populations.

For seniors considering or currently enrolled in Medicare Advantage, the Annual Enrollment Period (AEP) from October 15 to December 7 will be a crucial time to review all available options for 2026. Understanding the breadth of 2026 Medicare Changes to Part C plans will empower you to select the plan that best aligns with your health needs and financial situation.

Expected Modifications to Medicare Part D: Prescription Drug Coverage

Medicare Part D provides prescription drug coverage through private insurance plans approved by Medicare. These plans have varying premiums, deductibles, formularies (lists of covered drugs), and cost-sharing structures. The landscape of prescription drug coverage is constantly evolving, driven by pharmaceutical innovations, drug pricing debates, and legislative efforts to reduce out-of-pocket costs.

Significant 2026 Medicare Changes are anticipated for Part D, particularly in light of recent legislative reforms aimed at lowering drug costs for seniors. The Inflation Reduction Act (IRA) of 2022 introduced several key provisions that will continue to roll out through 2025 and beyond, culminating in substantial changes by 2026. One of the most impactful changes will be the implementation of a $2,000 annual out-of-pocket cap for Part D beneficiaries, effective in 2025. This cap will provide considerable financial relief for individuals with high prescription drug costs, setting a new precedent for beneficiary protection.

Furthermore, the IRA empowers Medicare to negotiate the prices of certain high-cost prescription drugs, a policy that will gradually expand over time. While the full impact of these negotiations on drug prices might not be immediately apparent across all drugs by 2026, it is a foundational change that aims to reduce overall drug expenditures for both Medicare and beneficiaries in the long term. This could lead to lower premiums for some plans or reduced cost-sharing for certain medications.

Formularies are another area that consistently sees changes. Pharmaceutical companies regularly introduce new drugs, and older drugs may lose patent protection, leading to generic alternatives. Part D plans update their formularies annually to reflect these changes, adding new medications, removing others, or altering their tier placement. Seniors should carefully review the 2026 formulary for their chosen plan to ensure their essential medications will still be covered and at what cost-sharing level. Any significant 2026 Medicare Changes to formulary coverage could prompt a plan switch.

The Part D deductible and various phases of coverage (deductible, initial coverage, coverage gap/donut hole, catastrophic coverage) are also subject to annual adjustments. While the IRA has already begun to reform the coverage gap, making it less of a burden, the specific cost-sharing percentages within each phase could still be tweaked for 2026. Beneficiaries should pay close attention to these figures to accurately estimate their potential out-of-pocket drug costs.

For low-income seniors, the Extra Help program (Low-Income Subsidy, LIS) assists with Part D premiums and costs. Any 2026 Medicare Changes could include adjustments to the eligibility criteria or benefit levels for the Extra Help program, potentially expanding assistance to more individuals or modifying the amount of support provided. Keeping informed about these programs is crucial for those who rely on them for affordable medication.

The cumulative effect of these Part D changes aims to make prescription drugs more affordable and predictable for seniors. However, the complexity of drug plans means that proactive research and comparison during the Annual Enrollment Period will be more critical than ever to ensure you have the most cost-effective and comprehensive coverage for your medications.

The Impact of Legislation and Economic Factors on 2026 Medicare Changes

The trajectory of Medicare is heavily influenced by legislative action and broader economic forces. Understanding these macro factors provides crucial context for the specific 2026 Medicare Changes that will eventually be implemented. Major pieces of legislation, like the Inflation Reduction Act of 2022, often have a multi-year phased implementation, meaning their full effects are felt years after enactment.

The IRA, as mentioned, is set to profoundly reshape Part D. Beyond the out-of-pocket cap and drug price negotiation, it also includes provisions for free vaccines (covered by Part D, like shingles vaccine) and limits on insulin costs. By 2026, these provisions will be fully integrated, offering substantial financial relief for specific healthcare needs. However, the long-term economic impact of these changes on the pharmaceutical industry and the broader healthcare market is still being assessed, and these assessments could, in turn, influence future policy decisions.

Economic conditions, such as inflation, interest rates, and the overall growth of the U.S. economy, directly affect Medicare’s financial health. Higher inflation, for instance, can increase the cost of medical supplies, equipment, and labor, thereby driving up the expenses for hospitals and other providers. These increased costs are often passed on to Medicare, potentially leading to higher premiums, deductibles, or coinsurance for beneficiaries. Conversely, periods of strong economic growth can lead to higher payroll tax revenues, which help to bolster the Medicare Trust Funds.

The Medicare Trustees’ Annual Report is a critical document that provides a snapshot of the program’s financial status and projections for the coming years. This report often highlights potential solvency issues and recommends policy adjustments. The findings of the 2025 and 2026 Trustees’ Reports will be instrumental in informing legislative debates and administrative decisions regarding the 2026 Medicare Changes. These reports are often a bellwether for where adjustments might be needed most, such as in Part A’s hospital insurance trust fund.

Political climate and upcoming elections also play a significant role. Healthcare is a perennial topic in political discourse, and proposed reforms to Medicare are frequently part of electoral platforms. Depending on the outcomes of elections leading up to 2026, there could be new legislative pushes for either expanding Medicare benefits, reforming its structure, or addressing its financial challenges through different means. These political dynamics can introduce an element of uncertainty but also opportunities for positive change for beneficiaries.

Furthermore, the ongoing evolution of healthcare delivery models, such as the shift towards value-based care and integrated health systems, could also influence Medicare policies. CMS continually explores ways to incentivize quality care outcomes over fee-for-service volume. Any new initiatives in this area could lead to changes in how providers are reimbursed, which could indirectly affect the services available to beneficiaries or the efficiency of care delivery under the 2026 Medicare Changes.

In essence, the 2026 Medicare Changes will be a reflection of the nation’s economic health, legislative priorities, and the ongoing effort to ensure Medicare remains a sustainable and effective program for all eligible Americans. Staying informed about these broader trends can help seniors understand the rationale behind specific policy adjustments and anticipate their potential impact.

Preparing for 2026 Medicare Changes: A Proactive Approach for Seniors

Given the certainty of some 2026 Medicare Changes and the potential for others, a proactive approach is essential for U.S. seniors. Waiting until the last minute can lead to confusion, missed opportunities, or even unexpected out-of-pocket costs. Here are key strategies to help you prepare effectively:

1. Stay Informed Through Official Channels

The most reliable information about 2026 Medicare Changes will come directly from official sources. Regularly check the official Medicare.gov website, sign up for email updates from CMS, and review any mailings you receive from Medicare or your current plan. These official communications will provide accurate details on premium adjustments, deductible changes, and modifications to covered benefits. Be wary of unofficial sources that may spread misinformation or try to sell you products based on inaccurate claims.

2. Review Your Current Coverage Annually

Even if you are satisfied with your current Medicare plan, the Annual Enrollment Period (AEP) from October 15 to December 7 each year is an invaluable opportunity to re-evaluate. Your plan’s benefits, costs, and formulary can change, and your health needs might also have evolved. For 2026, carefully review your plan’s Annual Notice of Change (ANOC) and Evidence of Coverage (EOC). Compare your current plan with other available options to ensure it still offers the best combination of coverage, cost, and provider access for your specific situation. This is especially crucial given the expected 2026 Medicare Changes to Part D.

3. Understand Your Healthcare Needs

Before comparing plans, take stock of your current and anticipated healthcare needs. List all your prescription medications, including dosages, and note any specialists you see regularly. Consider any upcoming medical procedures or chronic conditions that might require specific coverage. Having a clear picture of your healthcare requirements will help you identify plans that best meet those needs under the new 2026 Medicare Changes.

4. Utilize Medicare Resources and Counseling

Medicare offers several resources to help beneficiaries navigate their options. The Medicare Plan Finder tool on Medicare.gov allows you to compare plans side-by-side. Additionally, State Health Insurance Assistance Programs (SHIPs) provide free, unbiased counseling to Medicare beneficiaries. These programs have trained counselors who can help you understand the 2026 Medicare Changes, explain your options, and assist you in enrolling in a new plan if necessary. Don’t hesitate to leverage these invaluable resources.

5. Budget for Potential Cost Adjustments

As discussed, premiums, deductibles, and coinsurance amounts are subject to change. Factor potential increases into your annual budget. If you anticipate higher out-of-pocket costs due to 2026 Medicare Changes, start saving or adjust your financial planning accordingly. Understanding the maximum out-of-pocket limits for Medicare Advantage plans and the new $2,000 cap for Part D will help you manage potential expenses.

6. Consider Medigap (Medicare Supplement Insurance)

If you have Original Medicare, Medigap policies help cover some of the out-of-pocket costs not paid by Original Medicare, such as deductibles, copayments, and coinsurance. While Medigap plans themselves do not typically change annually in terms of benefits (they are standardized), the underlying Original Medicare costs they cover will be affected by the 2026 Medicare Changes. Reviewing your Medigap policy alongside potential Original Medicare adjustments is wise to ensure you still have adequate supplemental coverage.

7. Review Eligibility for Financial Assistance Programs

Many seniors may be eligible for programs like Extra Help (for Part D costs) or Medicare Savings Programs (MSPs), which help with Part B premiums and other costs. These programs have income and resource limits that are adjusted annually. If your financial situation has changed, or if you were previously ineligible, recheck your eligibility for these programs, especially in light of any 2026 Medicare Changes that might expand access or adjust thresholds.

8. Consult with a Trusted Advisor

For complex situations, consulting with a financial advisor, elder law attorney, or a licensed insurance agent specializing in Medicare can provide personalized guidance. They can help you understand how the 2026 Medicare Changes specifically apply to your circumstances and assist with long-term healthcare planning.

Conclusion: Navigating the Future of Your Healthcare with 2026 Medicare Changes

The upcoming 2026 Medicare Changes represent a natural evolution of a vital healthcare program designed to serve millions of U.S. seniors. While the specifics are still unfolding, the overarching themes will likely include adjustments to premiums, deductibles, and cost-sharing, along with refinements to covered services and significant reforms to prescription drug coverage. These changes are driven by a complex interplay of economic factors, demographic shifts, legislative priorities, and the continuous quest for healthcare innovation and efficiency.

For seniors, the key to navigating these adjustments successfully lies in proactive engagement and informed decision-making. By staying updated through official sources, diligently reviewing your current coverage, understanding your personal healthcare needs, and utilizing available resources like Medicare Plan Finder and SHIP counseling, you can ensure that your healthcare coverage remains robust and affordable.

Embrace the Annual Enrollment Period as your annual opportunity to reassess and optimize your Medicare plan. The 2026 Medicare Changes are an inevitable part of a dynamic system, but with careful planning and a commitment to staying informed, you can confidently secure the healthcare benefits you deserve. Your health and financial well-being are paramount, and being prepared for these changes is a fundamental step in safeguarding both.